|

KARACHI (July 05 2010): During the last week, weather has been quite favourable for cotton plant development. With the end of June month, even late cotton sowing is reported to have been completed. However, final figures about area sown to cotton is yet to be announced by the government but last year (2009-10) it was 3.106 million hectares and with 10 percent increase, it may be around 3.416 million hectares.

In July-September- 09 monsoon period, Pakistan received 101.8 millimeter rains against normal rain amount of 137.5 millimeters - 35.7 percent shortfall. This season (July - September 10) monsoons are predicted normal at 137.5 millimeters. For the last couple of seasons, shortage of irrigation water has been experienced in many areas specially tail-end areas partly because of shortage of water in canals and partly due to poor water management practices.

Some time back, when I talked to a cotton merchant in India and discussed the effects of monsoon rains on cotton crop, he had replied that normal monsoon rains would benefit cotton crop in India specially in Gujarat, Maharashtra, Karnatak and Andhara states of South and West India where largely dependence is on rains but same size rains may not benefit cotton crop in Pakistan because cotton crop in Pakistan is sufficiently irrigated by canal waters and rain waters extra.

In the last couple of seasons, it has been observed that even lesser than normal rains did not cause damage to cotton crop as much as normal to heavy rains do. These phenomena appeared to be justified in previous seasons when we had enough irrigation water supply for cotton crop but it is losing its relevance as irrigation water supply is decreasing and dependence on monsoon is increasing season by season. We hope a fairly good season with timely normal rains would help us harvest a bumper cotton crop of over 15,0 million bales.

Although number of operational ginning factories has increased to around 40 - more than 75 percent in Punjab and less than 25 percent in Sindh province, but it is increasing almost every day. Contrary to out-going cotton season, incoming one took lead over Sindh in resumption of ginning operation and also in quality of cotton. Punjab growers speak very high of the coming results of new Bt cotton varieties sown in Punjab in terms of higher yields and better cotton quality. This analyst is quite sure that Punjab province, having more than 2/3rd. of total cotton area, has great potential in increasing national cotton production and this time Punjab results may surprise us.

New crop arrivals are increasing and presently some 3,000 to 4,000 bales are being ginned and pressed daily. This time, Sindh style cotton is selling at lower rates than Punjab otherwise in previous seasons, Sindh style cotton commanded premium over Punjab quality. This shows that pattern has changed on introduction of Bt cotton varieties in Punjab. Seed-cotton prices have improved by about Rs200-300 per 40 Kgs and so the lint prices by about Rs 400 - 500 per 37.324 Kgs ex-gin. Seed-cotton prices have reached historical peak of Rs 3,200 per 40 Kgs while lint cotton prices touched the ever high level of Rs 7,100 per 37.324 Kg ex-gin both in Punjab while in Sindh prices are lower by some 200-250 and Rs 300-400 respectively.

About ten days back, prices for ready delivery bargain of lint cotton was quoted at Rs 6,300 ex-Haroonabad- Punjab. If we look back to the start of this out-going (2009-10) season, we find that it started with seed-cotton prices around Rs 1800 and lint cotton prices around 3,200-3,300 and finished at ever highest rate of 6,800 per 37.324Kg ex-gin but new crop season (2010-11) has taken start from seed-cotton prices of Rs 3,200 and lint cotton Rs around 6,500 per maund and has peaked at Rs 7,100 last week. As reported in previous reports, the incoming cotton season may be very tricky and risky in view of possible great uncertainties. Of course, old crop stocks have almost exhausted and new crop arrivals are falling short of domestic cotton demand but domestic yarn prices are lower and export parity of lint cotton is also lower than present level of domestic prices.

There is a question mark on preset increase of lint price over Rs 7000 per maund. The spinners as well the ginners fail to pin point the reason for this abnormal increase in cotton prices. One impression is that the export-oriented spinning mills are holding local sale of yarn in hope to get better price in export when 15 percent export duty on yarn expires on 26th instant. The value added sector has demanded of the government to extend this levy of 15 percent export duty on yarn for two months to enable the value added sector meet their export commitments.

The spinning sector is against any extension of this 15 percent export levy on cotton yarn. Second point is that larger spinning mills appear covered with their cotton requirements by August month, local as well as imported cotton while hand-to-mouth running mills are in the market for procurement of new crop lots and they do not want to face closure of their spinning operation only due to non-availability of raw cotton.

The larger groups / export-oriented spinning mills are trying to book foreign cotton to meet their cotton requirements up to September month. Third point is that in view of tight liquidity position, the spinning mills do not want to lower cotton and yarn prices to keep their valuation of pledged stock above their drawn credit and for increasing drawing power. Fourth point is that spinning mills are trying to avoid closure of mills as it costs more than the operating loss of couple of fortnights. One version is that if the government does not extend the 15 percent levy on export of cotton yarn beyond 26th instant, the domestic prices of lint cotton and cotton yarn may come under selling pressure.

The present level of seed-cotton prices and lint cotton prices do not appear even workable but the spinning mills do not want to close down operation for a fortnight or two. The general impression is that cotton prices may not go down in next month or so in view possible slowing down of cotton arrivals when monsoon starts. However, cotton prices may show downward trend in September month when cotton arrivals would increase and money demand would increase due to Ramazan and Eid festival. Overall impression about cotton market is that uncertainty would extend till government takes its decision regarding expiry or extension of 15 percent levy on export of cotton yarn. The value-added textile sector want regular and smooth supply of their raw materials for running this sector smoothly as this sector earns enough foreign exchange through value addition and employs major labour force.

China being production engine of textile products is the largest consumer of cotton yarn. In this season, Chinese larger import requirements of cotton, yarn and other textile products triggered world cotton and yarn prices to high levels world wise but more particularly in neighbouring countries like India, Pakistan, Bangladesh, Indonesia, Thailand and Vietnam. Lint cottons stocks lying in warehouses belonging to international merchants were once flooded, have almost dried out. The international merchants would like to keep sufficient cotton stocks in warehouse in China for prompt delivery.

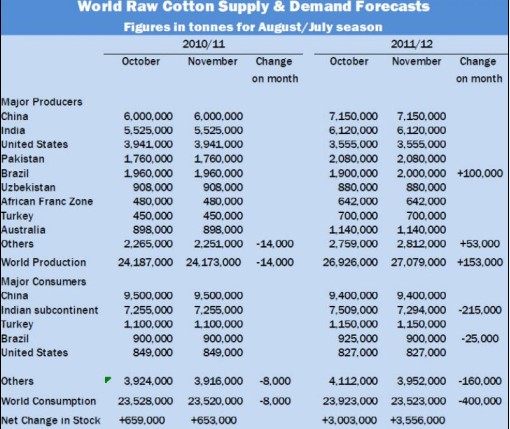

In 2010-11 season, world cotton consumption would increase by 2.067 million 480-lb bales and alone in China 1.500 million bales - about 75 percent of world increase. In 2010-11, world cotton production would increase by 12.427 million 480-lb bales while in China increase would be only 1.00 million bales. Thus, as compared to 2009-10 season, net availability of cotton in the world would increase by 10.36 million bales next season and perhaps the top beneficiary would be China.

Table No 2

|