|

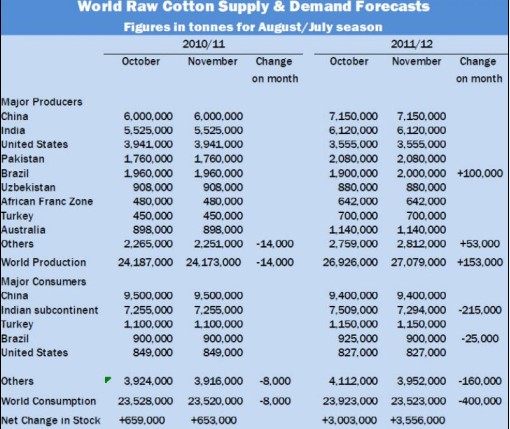

LAHORE (June 04 2010): After losing about Rs 1,200 per maund (37.32 kgs) over the last month, lint prices continued to nosedive in the domestic market due to our bearish fundamentals. Steeply high Regulatory Duty (RD) on yarn exports imposed on May 13, 2010, impending closure of some spindles till the arrival of the new crop (2010-2011), increasing the count number of yarns by the Pakistani mills and accumulation of yarn stocks due to notable decrease in yarn exports have joined together to plummet fiber prices precipitously. Though a negligible unsold stock of 20,000 to 25,000 local size bales of lint remains with the ginners from the current season (2009-2010), even then the cotton market is ominously quiet with scant a buyer as the spinners have been left the lurch with a very dull and dreary yarn market where offtake is down considerably. Moreover, the federal budget for the incoming fiscal year (July 2010 - June 2011) is due for announcement on the 5th of June 2010, which has further put regular economic activity on the back burner. Stray ready sales of 400 bales of cotton from Khanpur in Punjab at Rs 6450 per maund (37.32 kgs), possibly on credit, or 400 bales from Burewalla at Rs 6400 per maund in Punjab have been reported over the past couple of days, but general price range has been much lower extending from Rs 5500 to Rs 6200 per maund according to the quality. Traditionally, some domestic new cotton crop sales commence in March or April of each year for forward deliveries in June, July or even August, but due to a host of difficulties and uncertainties surrounding the textile business, and also the impending federal budget due at the end of this week, no credible forward sales of the new crop have been reported in the market. Preliminary ideas indicate that a modest quantity of new crop (2010-2011) from Punjab may start arriving from the middle or the end of June 2010, but Sindh styles would arrive later due to water shortages which were reported earlier from that region. Of course larger quantities may not arrive till August 2010. The outgoing season (2009-2010) has been earmarked to end up with an output of 12.7 million domestic size bales on an ex-gin basis. New crop (2010-2011) cotton output is being projected between 13.5 to 15 million domestic size bales on an ex-gin basis, though some estimates put it much higher. Regarding Pakistani mills consumption, it is being estimated to range between 14.5 million to 14.75 million domestic size bales during the current season, while consumption for the forthcoming season is being presently projected anywhere from 15.25 to 15.5 million of local size lint bales. Imports of further cottons have gone down due to tight physical availabilities from various global origins for nearby shipments, even though new crop price ideas have somewhat decreased in the futures market (ICE), but that would be considered later by the Pakistani spinners. Pakistani spinners suffered a setback when Indian government imposed restrictions of cotton exports which problems have still not been fully settled or resolved. Moreover, the imposition of a stern Regulatory Duty (RD) on yarn exports from Pakistan has further undermined the performance of the Pakistani spinner. Both the Indian move to clamp down on cotton exports and the Pakistani decision to impose Regulatory Duty on yarn exports militate again the free trade mechanism. Therefore, regional cotton trades and textile businesses in both India and Pakistan have been unnecessarily disrupted and put in disarray. These steps also go against the interest of the growers in both the countries. The Pakistani rupee has also sunk to its record low level at 85 units against the United States dollar. This may be good for exports, but it will also discourage the import of much needed capital machinery for modernisation and development. On the global economic and financial front, once again the fear has arisen that we are heading towards a double dip recession. On the net analysis, more bad data and news of further fraud and malpractices by leading business corporations have come to the fore. Above all, credit rating agencies like the Moody's have come under enquiry and investigation regarding their propriety in providing honest services to the investors around the world. Further fear has been ignited with the realisation that government kitties and their powers to dole out bailout moneys have reached the end of the tether. Now sovereign debt problems are haunting many countries around the world. Moreover, besides Greece, Ireland, Spain, Portugal and Italy, it is now being feared that even France may be facing more economic and financial problems than envisaged earlier. Some observers have also started thinking if Germany will be turning its back on the Euro zone and leave it in the lurch. Thus, if any thing, week by week, month by month and year by year, the economic and financial condition of most countries around the world are worsening. No Keynes has yet emerged to give us new solution to the ever increasing complex trade, economic and financial problems around the globe. What we need is a New Global Dispensation (NGD) which can integrate the sundry social, economic and financial needs of the world in one grand and equitable proposition. |

|

Cotton prices continue to sink

Updated: 2010-6-4 Source: Texglobe-信息中心

Recommended News

Photo Gallery

Most Popular