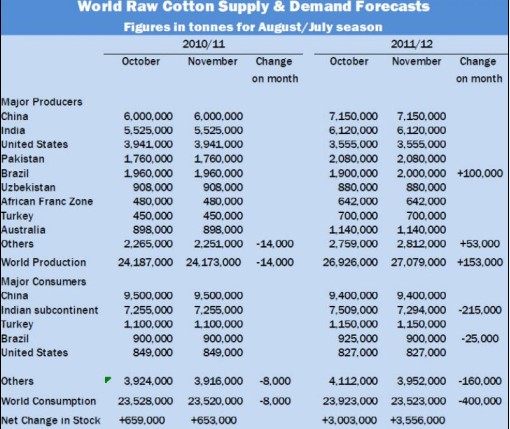

|

LAHORE (December 24, 2010) : Following its own fundamentals and also taking cue from the capricious New York futures market, cotton prices depicted a poor performance in the local market. Lint prices shed nearly Rs 500 per maund (37.32 Kgs) from the overnight rates and performed sluggishly ahead of the spate of forthcoming holidays including the birthday of Quaid-e-Azam Mohammed Ali Jinnah, the founder of Pakistan, which is also Christmas day, in addition to other attached holidays at the end of the calendar year and the beginning of the New Year (2011) thereafter. Thus seedcotton (Kapas/Phutti) prices reportedly ranged lower in both Sindh and Punjab on Thursday from Rs 3,900 to Rs 4,200 per 40 kilogrammes. Similarly, lint prices showed a significant decrease in both Sindh and Punjab and are said to have extended from Rs 8,900 to Rs 9,300 per maund (37.32 Kgs). The New York cotton futures market (ICE) has behaved quite agitatingly and aberrantly over the past several weeks and thus one can hardly swear by its inconstant behaviour, fundamentals or no fundamentals, technicals or no technicals. Just a couple of days ago (21st December, 2010), it recorded an historic high rate of US Cents 159.12 per pound for the key March 2011 contract, only to plunge by 10 or 11 cents per pound on Thursday. This performance by ICE appears fickle and consequently also hazardous for both buyers and the sellers. The inconsistent and suspenseful Indian cotton export policy is also adding a considerable amount of uncertainty to global exports of the commodity. Now we learnt that from the 5.5 million bales of cotton which had been registered for export earlier and from which an estimated three million bales had been shipped, now the government of India has indicated that it would open up registrations for an expected 2.5 million bales presumably in January, 2011. In the meantime, yarn markets are reported to be slow moving with reduced offtake. New York Cotton futures (ICE) market will be closed on 24th December, 2010 with the following two days remaining closed statutorily. We may thus witness less fireworks in the period starting from now till almost the beginning of next year (2011) when regular business may resume on an appreciable scale, but nothing may be said with any certainty. Under these circumstances, buyers of cotton have mostly withdrawn in both New York and for several physical cottons at their origin and are presently showing some resistance. Yarn offtake is also down comparatively and fabric markets are also reportedly sluggish. In fact, in some mills yarns are stated to have started accumulating because the yarns are not selling satisfactorily. Uncertainties continue to abound with little guageable direction on the possible behaviour of cotton and yarn markets as seen here. Paucity of credit at the end of the calendar year is also restraining any impressionable activity for the time being. According to current reckoning, Pakistan may produce between 10.5 million to 11.25 million domestic size bales during the current season (August 2010 - July 2011) on an ex-gin basis. From this output projection, exporters may be able to ship about half a million bales. Mills would thus need to import between 2.5 million to three million bales (170 Kgs) this season. Ready cotton sale business remained lacklustre on Thursday. A sale of 100 bales of cotton from Sultanabad was reported in Sindh at Rs 8950 per maund (37.32 Kgs), 200 bales from Jhol sold at Rs 9,000 per maund, while 400 bales from Upper Sindh (K-68) were said to have been sold at Rs 9,300 per maund. In the Punjab, 200 bales from Chichawatni were sold at Rs 9,000 per maund. Several holidays over the next fortnight muted the buying mood of many of the mills. Cotton imports and bookings into Pakistan are variously estimated to range from one million to 1.5 million bales (170 Kgs) till now. From these figures, about half a million bales have already reached Pakistan. On the global economic and financial front, equity prices have generally increased with Dow Jones reportedly showing two-year high levels and Standard and Poor is said to be posting close of pre-Lehman Brothers level when Lehman went bankrupt two years ago. These performances appear to be the result of continued easing of money flooding the markets in much of Europe and America with uninterrupted cash. Therefore, the name of the game remains continued splashing of cash to the consumers, maintaining or renewing bailout schemes and slashing income taxes, including for the rich. The question remains how most of the governments will pay back all the loans they are accumulating and sovereign debts they are creating without restraint. Eurozone economies remain vulnerable while United Kingdom is still performing poorly. The growth rate of United Kingdom has been revised downwards for the third quarter with portents of a sharp downturn being projected for next year. Japan's economic growth is said to dwindle by half during 2011-2012 due to lower exports and high consumption. At midweek, the Greeks were protesting against the 2011 austerity budget. Inflation in China continues to be a serious concern for the managers of its economy. The only truth which seems to have emerged from the crumbling economic condition in most of the European countries, the United States and elsewhere is that a new block of emerging economies has arisen which has factually changed a sizeable part of global political, economic and financial clout in their favour. China seems to be the new role model, but economies like Brazil, Russia, India and Australia have also risen remarkably or promise better performance.

|

|

Weak showing on cotton market

Updated: 2010-12-24 Source: Business Recorder

Recommended News

Photo Gallery

Most Popular